Investors From Stocks to Crypto Brace for US Election Volatility

“Election volatility premium is most pronounced in the bond market on long-end rates, which we believe

reflects concerns over higher fiscal risks on a sweep outcome,” said Tanvir Sandhu, Bloomberg

Intelligence’s chief global derivatives strategist. “The skew suggests demand for hedges using payer

swaptions against a selloff in long-end rates.”

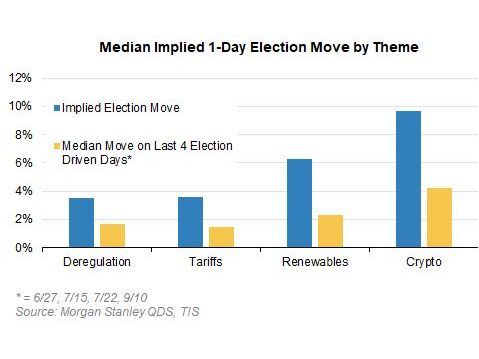

Crypto traders are diverging on the election result, with the options market turning from aggressively

bullish to a more hedge-focused approach. The implied volatility for short-term contracts such as the

14-day puts has risen significantly while calls with the same expiration remain stable, according to

data compiled by crypto liquidity provider B2C2.

While there is no clear directional bias with heightened volatility going into the election, increasing

premium for calls across longer tenors and termed Bitcoin futures on CME point to a bullish outlook

beyond the election, with more rate cuts and potential positive changes in crypto policies in sight next

year.

Cross-Asset

Binary options — in which a payout is triggered if a pair of conditions are met, such as a currency and

a stock reaching pre-determined levels — tend to be a popular way to hedge possible outcomes around

major events. Such trades have picked up going in the election, according to Esmail Afsah, a derivatives

strategist at JPMorgan.

“I suspect this is mainly because investors have firm views on how individual assets are likely to

behave in the four key permeations of the US election,” Afsah said. “Using hybrid options and betting on

the direction of two assets concurrently allows to increase leverage materially and thus improve odds,

providing of course that assets do indeed behave as expected.”

—With assistance from David Pan, Christian Dass, Jessica Menton and Jan-Patrick Barnert.